Affordable housing (किफायती आवास योजना) is one of India’s most critical development goals. With urban migration, rising property prices, and income disparities, owning a safe and permanent home remains a challenge for millions. To address this, the government has introduced multiple housing programs at both central and state levels.

Understanding PMAY vs State Housing Schemes (पीएमएवाई बनाम राज्य आवास योजनाएं) is crucial for citizens, policymakers, and developers. While both aim to provide affordable housing (किफायती आवास योजना), their eligibility criteria, funding models, and benefits differ significantly.

Pradhan Mantri Awas Yojana – PMAY (प्रधानमंत्री आवास योजना)

Objectives of PMAY (प्रधानमंत्री आवास योजना के उद्देश्य)

PMAY was launched with the mission of “Housing for All (सबके लिए घर)”. Its goals include:

- Reducing housing shortages nationwide

- Promoting low-income housing (कम आय वर्ग आवास) and middle-income housing (मध्यम आय वर्ग आवास)

- Ensuring women’s ownership of property

- Supporting inclusive and sustainable urban development

Components of PMAY: Urban (शहरी) and Rural (ग्रामीण)

- PMAY-Urban (PMAY-U / शहरी)

Focuses on urban housing (शहरी आवास योजना) for EWS, LIG, and MIG categories. - PMAY-Gramin (PMAY-G / ग्रामीण)

Targets rural families living in kutcha or unsafe houses to promote rural housing (ग्रामीण आवास योजना).

Both components aim to provide houses with basic amenities such as water, sanitation, and electricity.

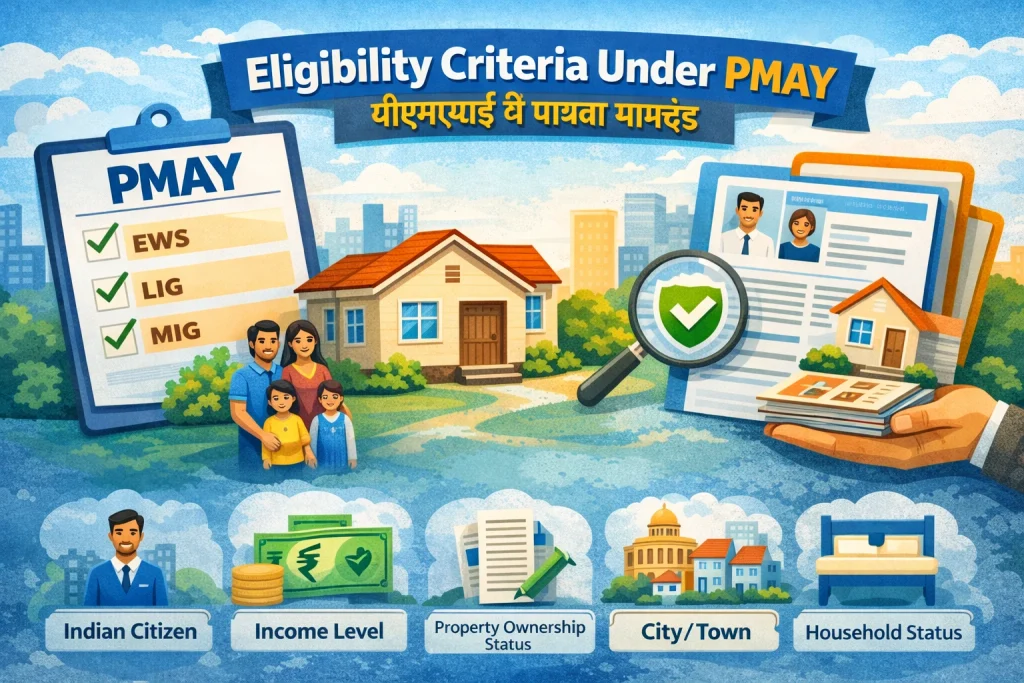

Eligibility Criteria Under PMAY (PMAY पात्रता)

- EWS (आर्थिक रूप से कमजोर वर्ग): Up to ₹3 lakh annual income

- LIG (निम्न आय वर्ग): ₹3–6 lakh annual income

- MIG-I & MIG-II (मध्यम आय वर्ग): ₹6–12 lakh & ₹12–18 lakh annual income

Other criteria:

- Must not own a pucca house anywhere in India

- Female ownership or co-ownership is mandatory or preferred

Overview of State Housing Schemes (राज्य आवास योजनाएं)

Purpose of State-Level Housing Programs (राज्य स्तर की योजनाओं का उद्देश्य)

State housing schemes (राज्य आवास योजनाएं) address region-specific challenges (क्षेत्र-विशेष आवास समस्याएं). They consider land availability, climate, local population density, and economic conditions.

Examples of Popular State Housing Schemes (लोकप्रिय राज्य आवास योजनाएं)

- MHADA Housing Scheme (महाराष्ट्र)

- Tamil Nadu Housing Board (TNHB / तमिलनाडु)

- Telangana 2BHK Housing Scheme (तेलंगाना 2BHK योजना)

- Banglar Bari (West Bengal / पश्चिम बंगाल)

Eligibility Criteria Under State Housing Schemes (राज्य योजना पात्रता)

- Local residency requirements

- Caste/community-based benefits

- Occupation-specific support (e.g., construction workers)

State schemes are more flexible than PMAY, making them accessible for specific local groups.

PMAY vs State Housing Schemes (पीएमएवाई बनाम राज्य आवास योजनाएं): Structural Differences

Centralized vs State Governance (केंद्रीकृत बनाम राज्य शासन)

- PMAY: Centralized guidelines issued by Union Government; states implement.

- State Schemes: Fully managed by state governments with flexible rules.

Funding and Cost-Sharing Models (फंडिंग और लागत साझेदारी)

- PMAY: Cost shared between Centre and State; includes loan subsidy (होम लोन सब्सिडी)

- State Schemes: Funded primarily by state budgets; may include grants or low-cost units

Flexibility in Design and Implementation (डिज़ाइन और कार्यान्वयन में लचीलापन)

State schemes allow customization of house size, layout, and location. PMAY maintains standardized norms across India for quality and monitoring.

Financial Benefits Comparison (वित्तीय लाभ तुलना)

Interest Subsidy Under PMAY (होम लोन सब्सिडी)

PMAY’s Credit Linked Subsidy Scheme (CLSS / क्रेडिट लिंक्ड सब्सिडी योजना) reduces EMIs for eligible families:

- EWS / LIG: Up to 6.5% interest subsidy

- MIG-I & MIG-II: Up to 4–3% interest subsidy

This makes middle-income housing (मध्यम आय वर्ग आवास) more affordable.

Direct Subsidies in State Housing Schemes (आवास सब्सिडी)

State schemes often provide direct grants (प्रत्यक्ष अनुदान) or low-cost housing. Interest subsidies are less common.

Target Beneficiaries and Coverage (लक्षित लाभार्थी और कवरेज)

Urban vs Rural Focus (शहरी बनाम ग्रामीण)

- PMAY: Balanced coverage for both urban and rural areas

- State Schemes: Focused on local priorities, e.g., slum redevelopment or rural housing

Income Groups and Social Categories (आय समूह और सामाजिक वर्ग)

- PMAY: EWS, LIG, MIG families

- State Schemes: Often target economically weaker sections, SC/ST, minority groups

Implementation, Transparency, and Monitoring (कार्यान्वयन, पारदर्शिता और निगरानी)

- PMAY: Uses geo-tagging and online dashboards for progress tracking

- State Schemes: Transparency varies; depends on state administrative capacity

Advantages and Limitations of PMAY (PMAY के लाभ और सीमाएं)

Advantages (लाभ):

- Nationwide uniformity

- Interest subsidies for home loans

- Strong monitoring and accountability

Limitations (सीमाएं):

- Strict eligibility rules

- Possible delays in approvals

Advantages and Limitations of State Housing Schemes (राज्य योजनाओं के लाभ और सीमाएं)

Advantages (लाभ):

- Localized and flexible

- Faster implementation in some states

- Community-specific targeting

Limitations (सीमाएं):

- Limited funding

- Quality may vary across regions

Which Housing Scheme Is Right for You? (कौन सी योजना आपके लिए सही है?)

Choosing between PMAY vs State Housing Schemes (पीएमएवाई बनाम राज्य आवास योजनाएं) depends on:

- Income level (आय स्तर)

- Urban or rural location (शहरी या ग्रामीण)

- Access to loans and subsidies (होम लोन और सब्सिडी)

Tip: Middle-income families may benefit more from PMAY’s loan subsidies, while low-income rural families may find state schemes more accessible.

Official updates: Ministry of Housing and Urban Affairs

Frequently Asked Questions (FAQs / अक्सर पूछे जाने वाले प्रश्न)

No, beneficiaries usually cannot avail benefits from two schemes simultaneously.

PMAY is centralized with interest subsidies; state schemes provide localized benefits and direct assistance.

Most state schemes offer direct grants rather than interest subsidies.

Yes, female ownership or co-ownership is mandatory or preferred.

No, limits vary by state and scheme.

State schemes may be faster due to localized administration.